ELTIF funds are, without question, the major evolution of the private market in 2025. But where do we stand? What should we expect next? Is this the new standard for private markets?

That’s what we’ll explore in this new edition of Owners Insights.

What is ELTIF 2?

In short, ELTIF 2 is the overhaul of the European framework created in 2015 to channel savings into the real economy — SMEs, mid-cap companies, and infrastructure projects.

Effective since January 2024, this new version simplifies and relaxes the original regime:

- Much broader access for retail investors,

- Removal of entry thresholds and liquidity constraints,

- Possibility to create evergreen ELTIFs,

- Greater flexibility in portfolio composition and share distribution.

The European Commission’s goal is clear: to make ELTIF 2 a trusted label that democratizes access to private assets and channels savings toward the real economy.

According to the Draghi Report, Europe will need to mobilize nearly €800 billion per year to finance the energy transition, strengthen its defense, and remain competitive in the global race for artificial intelligence.

What Has Changed Since 2024?

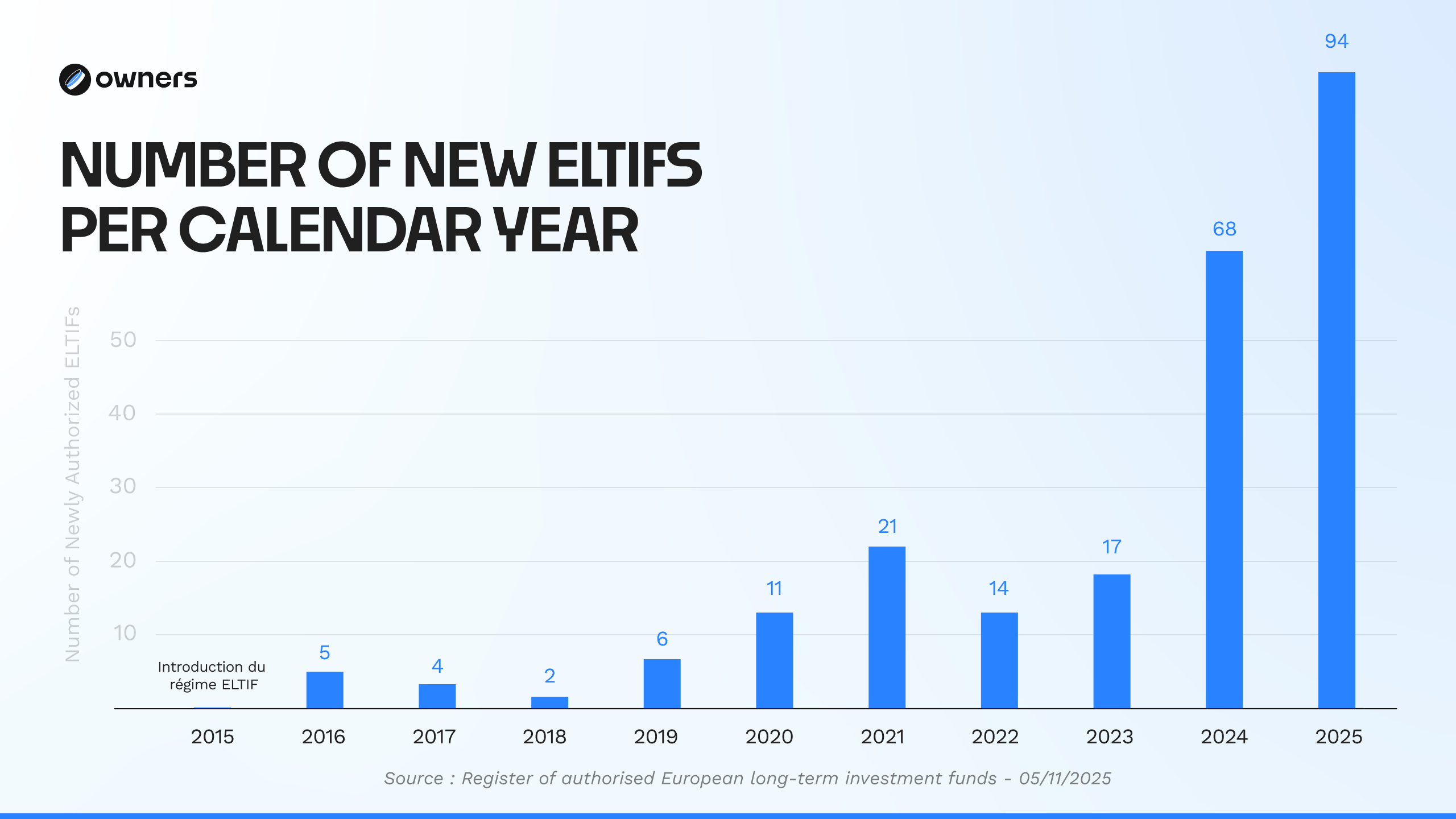

Since the implementation of version 2.0 in 2024, ELTIF has truly found its purpose. The market has grown by 300% following the new version, then by another 38.24% between 2024 and 2025 — reaching 162 ELTIF 2-labelled funds by the end of 2025.

In other words, asset managers have finally grasped the full potential of the regulation. After interviewing managers from various backgrounds, one thing stands out: the reasons for choosing the ELTIF label are highly diverse. For some, its greatest strength lies in the low minimum ticket. For others, it’s the European passport. For others still, it’s the flexibility of eligible assets.

Ultimately, the decision depends above all on the size of the investment platform — and therefore on its capacity to deploy capital quickly and to invest in commercial and marketing capabilities across multiple countries.

Who’s Driving the Market?

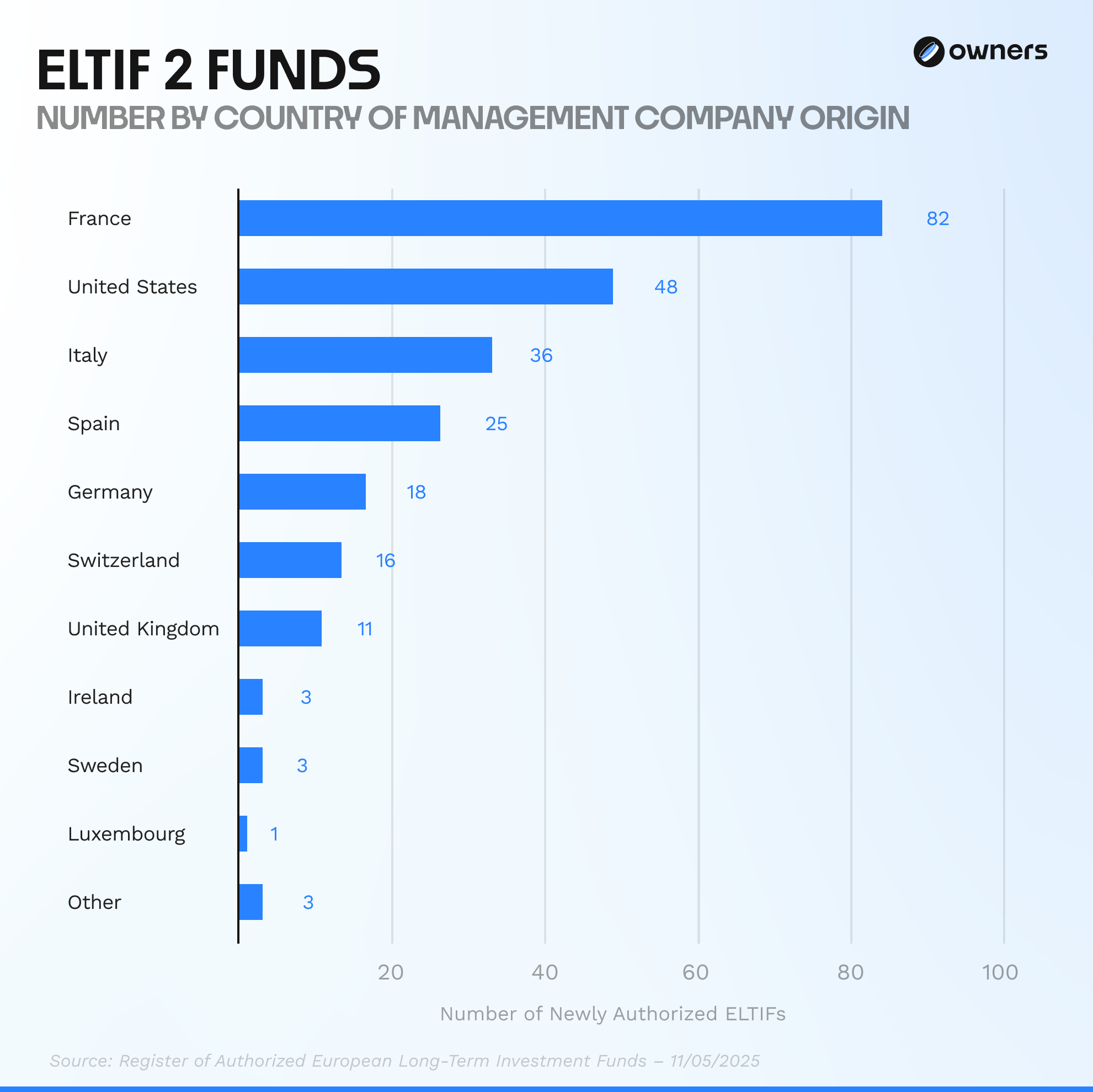

The main drivers behind ELTIF creation are French asset managers and their subsidiaries. Out of 162 funds, 82 originate from France: 43% are dedicated exclusively to retail investors, 42% to professionals, and 15% are mixed.

This breakdown reflects a market primarily using ELTIF for its flexibility on underlying assets and its low entry ticket. French management companies — in a country where 35% of household wealth is held in life insurance — have a major interest in making professional ELTIFs accessible to all through insurance-based distribution. Yet mobilizing that channel remains a significant challenge for most managers.

Luckily for them, it’s almost impossible to do so without a local management company…

Next come American firms and their European subsidiaries, with 48 funds — 53% serving both retail and professional clients, and 38% targeting professionals only. Here, ELTIFs serve a different purpose (more on that below). These U.S.-linked entities distribute their funds across an average of 18 countries. By contrast, all non-U.S. ELTIFs have an average of 4 countries and a median of 1, with a standard deviation of 5.4.

The United States is followed by Italy with 36 funds, Spain with 25, and Germany with 18.

A Two-Tier Ambition

The market is split into two distinct categories.

On one side, mid-sized European players seeking to kickstart their retailization. They design products accessible to all investors, with investment strategies tailored to the general public.

On the other side, the European subsidiaries of U.S. giants. They use the ELTIF passport to accelerate their European expansion and replicate their domestic retail model, launched back in 2020 after the SEC reform on “accredited investors”. That reform opened evergreen private market funds to retail investors.

In the U.S., pioneers such as Apollo, KKR, Hamilton Lane, and Blackstone led the way. Today, those same names top the ranking of ELTIFs authorized in the largest number of EU countries. Their ambition is clear: to apply their U.S. interstate model to the European market — treating each country as a separate state.

To achieve this, they are investing heavily and locally in marketing and sales forces, building on-the-ground networks of distributors — while gradually integrating their funds into tax-advantaged vehicles such as life insurance.

However, France has likely not had its final say. Whether it’s Eurazeo or Tikehau — two long-standing pioneers of retailization — or even Altaroc, which has made its mark in recent years, their intent is clear. They aim to expand across Europe through the union of capital.

The question remains: will they invest enough and leverage their local expertise effectively? Time will tell...

In the meantime, you can find all these funds on Owners — to compare, track, and analyze them. And follow us on LinkedIn to stay up to date with the latest developments in the sector.

For a deeper, more regulatory perspective, read the analysis by Valentine Baudouin (Regvantage) on the topic — [access here].