Evergreen: the word is on everyone’s lips in the private markets world. But what are we really talking about? Where does this model come from? What should we expect from it? How should we think about it?

We’re breaking it all down in this first edition of the Owners blog — the reference platform dedicated to private markets.

Is it new?

Despite what many in Europe might think, evergreen funds have existed in the United States since 1940 (yes, that’s a while ago — you probably weren’t born yet), and you all know at least one of them.

The first were Business Development Companies (BDCs) or investment holdings — think Berkshire Hathaway (yes, yes, Warren Buffett’s fund), founded precisely in 1940. Their model was simple: raise capital, list the fund on the stock market, and generate performance.

Then in the 1970s came the closed-end fund model, based on capital calls — initially designed for venture capital, standardized by Kleiner Perkins, Sequoia, and Bessemer, and later expanded to all strategies.

A few decades later, by the late 1990s, the evergreen model made a strong comeback among Family Offices, CVCs, and institutional investors who wanted to free themselves from the constraints of closed-end funds and focus more on long-term compounding.

Since 2010, this trend has only accelerated across geographies and structures — led by pioneers such as HarbourVest, Partners Group, Ares, Blackstone, KKR, and Apollo.

A marginal segment?

What share does this model hold in today’s global landscape? A tough question in a world that remains largely opaque.

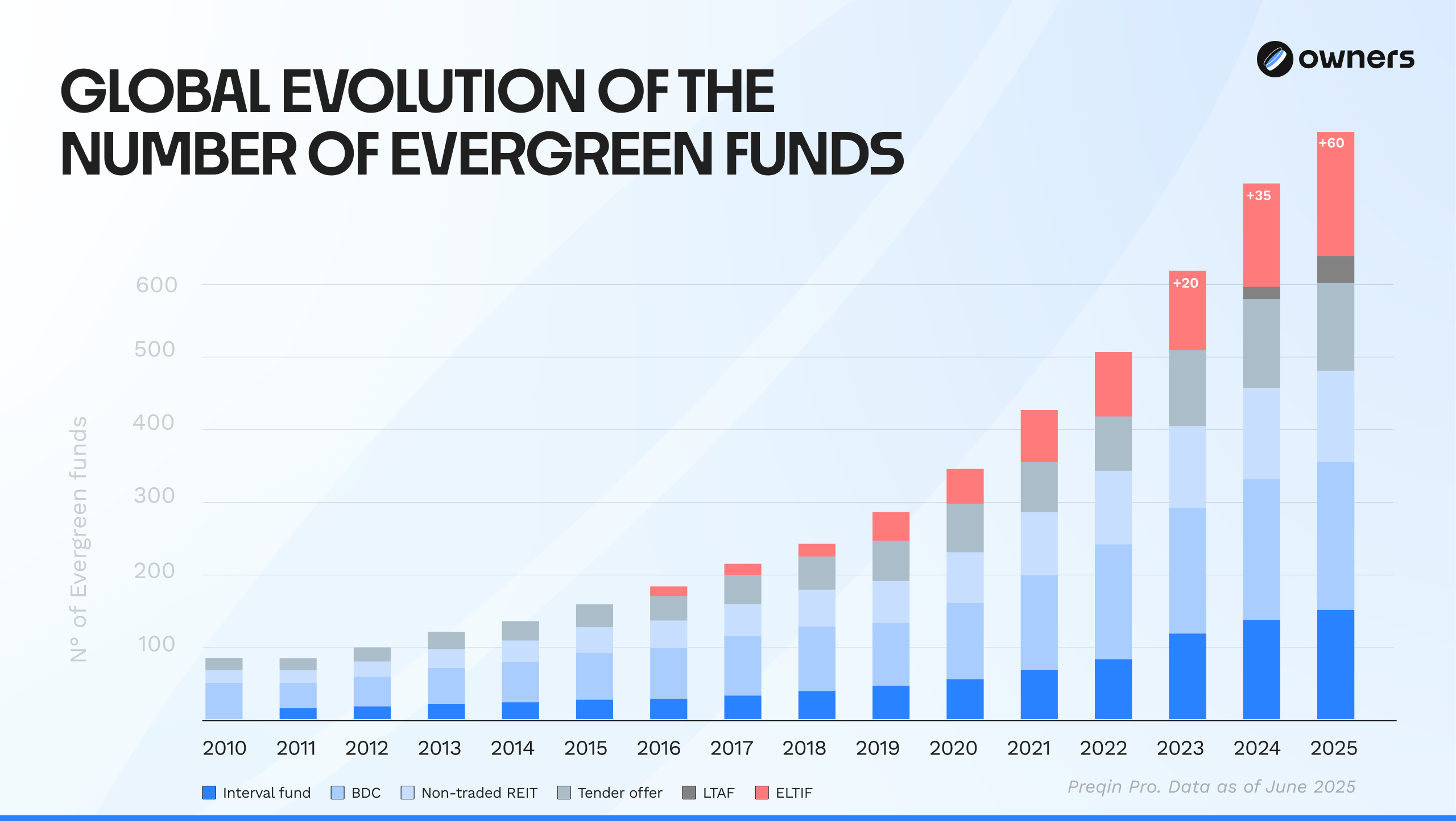

Out of an estimated USD 15 trillion in total assets (according to S&P Global), evergreen funds (excluding ELTIFs and LTAFs) represent USD 419 billion in assets under management — that’s 2.8% of the market, according to Preqin — roughly equivalent to Johnson & Johnson’s market capitalization.

PitchBook places the figure slightly higher, at USD 427 billion (including all private evergreen vehicles, of which USD 110 billion are interval and tender-offer funds), and projects the market to surpass USD 1 trillion by 2030.

Hamilton Lane, in its 2025 report, estimates the evergreen market at nearly USD 700 billion — about 5% of the total — and expects evergreen structures to reach 20% of the market by 2030.

The model remains marginal for now, but momentum is clearly building, driven by the wealth segment and the broader democratization of private markets. Leading players such as Apollo, KKR, Blackstone, Ares, and Partners Group are shaping this growth. The segment is expected to reach between 10% and 20% of total market share within the next five years.

Is it suitable for all strategies?

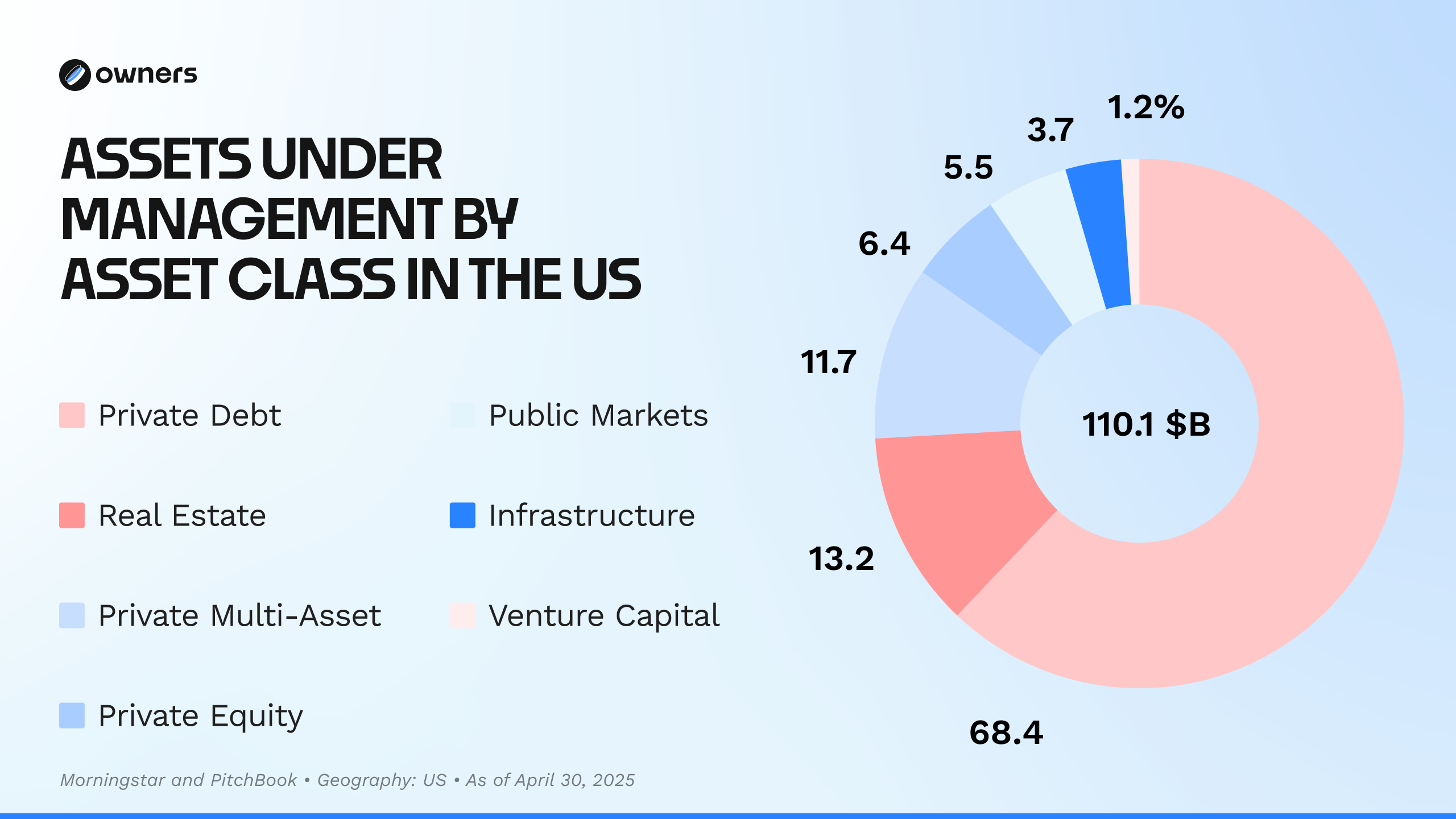

Are all asset classes treated equally? Evergreen structures don’t seem to fit all strategies perfectly. According to the latest Morningstar data on U.S. evergreen funds, private debt dominates the market, accounting for 68.4% of total assets.

This is largely due to the predictability of NAV volatility and the manageable liquidity it offers. In addition, the ability to either reinvest or distribute income makes it particularly suited to wealth management.

However, private equity, real estate, and infrastructure appear set to gain significant traction in the coming months, based on the latest insights shared on Owners.

Who dominates in Europe?

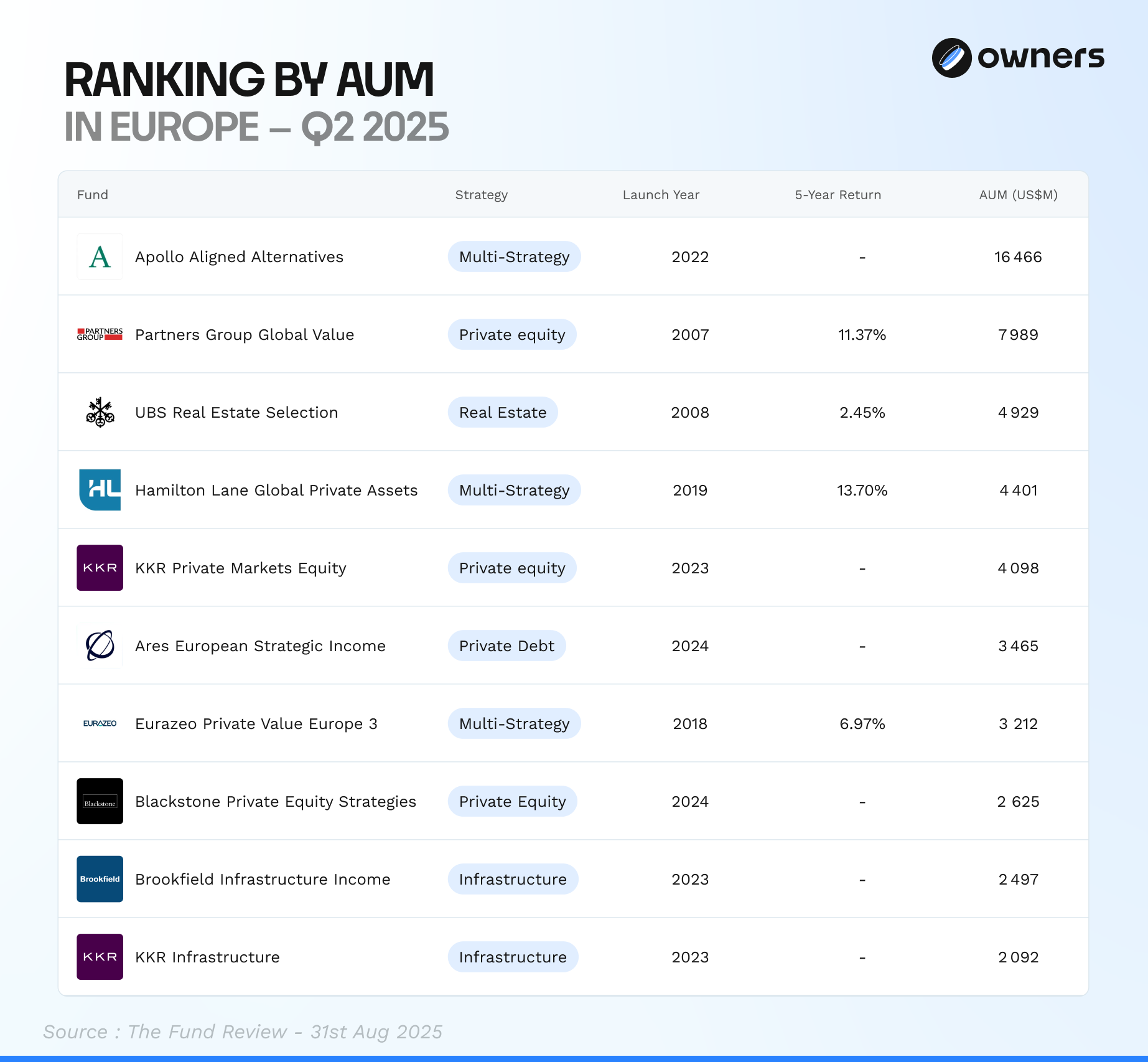

The European market is largely dominated by foreign players. Leading the pack is Apollo Global Management, with $16.5 billion in assets under management, followed by Partners Group with $8.0 billion, and UBS with $4.9 billion concentrated in its real estate vehicle.

The first player originating from the European Union only appears in seventh place: Eurazeo Private Value Europe 3 (EPVE 3), managing $3.2 billion in assets.

This market has been taking shape since the creation of ELTIFs and has accelerated since 2024 with ELTIF 2.

The main current distribution channels are Luxembourg life insurance and private banks, as most of these funds are SICAV Part II, meaning they are reserved for professional investors.

Moreover, the growing inclusion of evergreen funds in French life insurance — a market totaling €2.02 trillion in assets as of January 1, 2025, representing 35% of French household wealth according to France Assureurs — is expected to further boost this momentum.

So what should we make of it?

What lessons can we draw?

One thing is clear: the European model is still in its early stages, but its outlook is promising. However, it remains young, and the lack of reliable, well-documented, and consistent data for benchmarking is still its main weakness.

To the question, “Will evergreen funds replace closed-end funds?”, the answer is clear: no. Each structure has its own significant strengths and weaknesses, making them incomparable and suited to very different investor needs.