Since 2022, defense financing in Europe has emerged as a major strategic pillar — with space taking center stage.

Driven by two decades of gradual privatization and an ever-increasing dependence on hyperconnectivity, the space sector has become a core lever of technological and geopolitical sovereignty.

Much has been said about the New Space. But what does it actually mean? How is this sector financed? And above all, what investment opportunity lies behind this new space race?

What is the New Space?

When we talk about SpaceX and its satellite constellation, Blue Origin and its next-generation launchers, or Rocket Lab and its micro-launchers, we’re talking about the New Space: a privatized, agile, and commercial space industry.

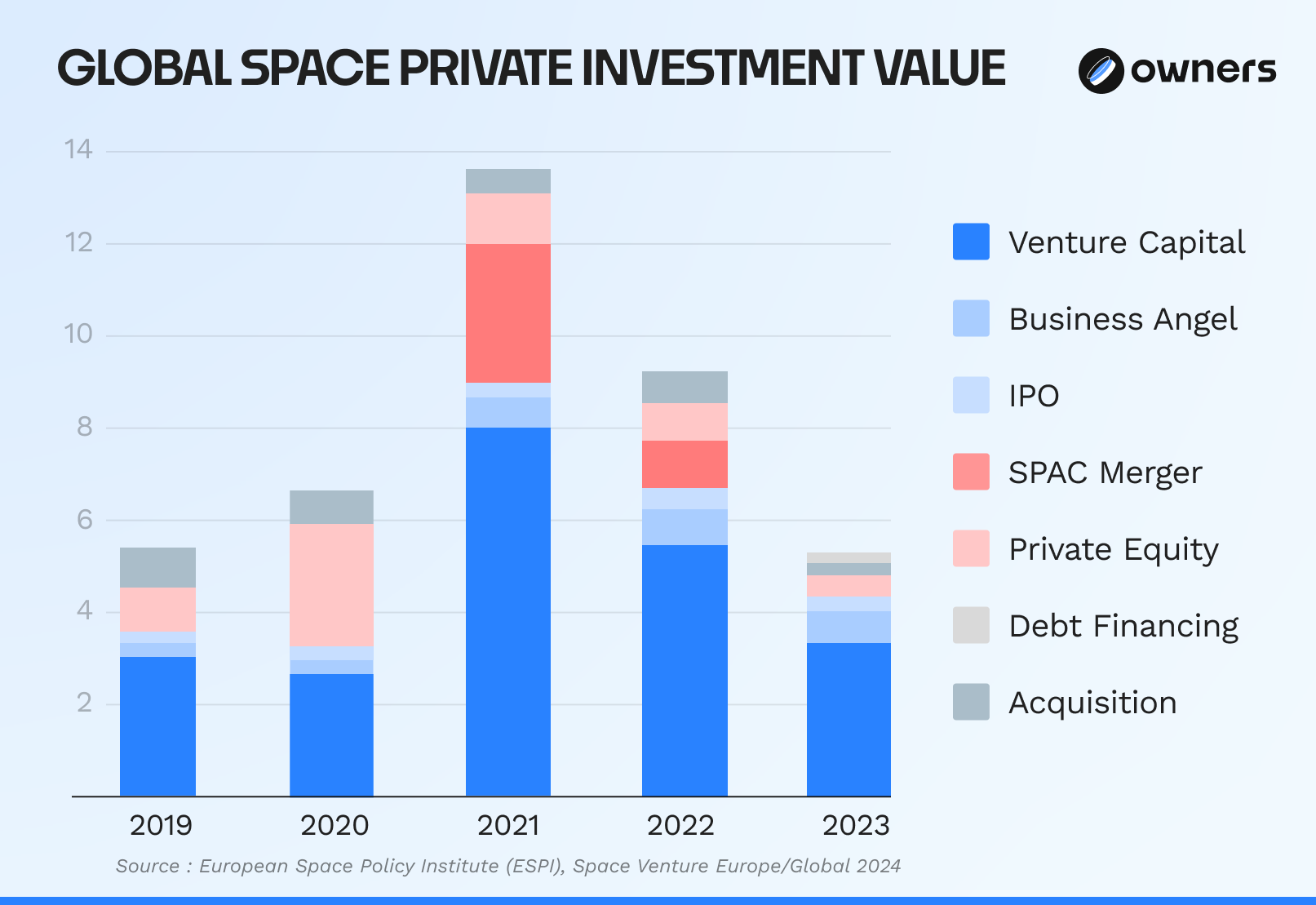

This is a global market valued at €411 billion in 2023, with €106 billion coming from public investment and €305 billion from the private sector — across the entire upstream (launchers, orbital infrastructure) and downstream (applications, services, data) value chain.

According to the European Space Agency (ESA), the sector recorded an average annual growth rate of 7–8% between 2018 and 2023. McKinsey projects that the market could reach $1.8 trillion by 2035, driven by the expansion of satellite constellations, the development of in-orbit services, and the growing fusion between civil and military uses of space.

.png)

An essential industry?

The gradual privatization of the space industry is far from neutral. Beyond the obvious gains in productivity and innovation, it raises a critical issue: the independence of our data.

Space has become a key geopolitical arena — a domain of informational sovereignty. Telecommunications, internet, GPS signals, air traffic management, weather monitoring, and even agricultural operations all rely on orbital infrastructure.

All these data flows pass through satellite constellations, increasingly under private control (SpaceX, Amazon, BeiDou, etc.).

Ensuring European sovereignty in this field has become a strategic imperative — a major challenge when the United States dedicates 0.24% of its GDP to the space sector, compared with only 0.09% in France.

.png)

This dynamic could reverse in the coming years, driven by the resurgence of European public investment through strategic programs such as IRIS², and even more by the rapid privatization of the space sector.

Venture capital funds have now become its main growth engine — accounting for 71% of private space financing in 2023, according to ESPI. This momentum is fueled by the pursuit of technological sovereignty, the search for exponential growth, and the promise of superior returns in dual-use markets, operating at the crossroads of civil and defense applications.

Expansion – unlocking Europe’s potential

It is within this momentum that Expansion was founded — a French asset management company managing €200 million in assets by the end of 2025.

Its mission: to foster European leaders in space and defense and strengthen Europe’s technological sovereignty.

With its first fund, already holding 24 portfolio companies and having completed an exit (The Exploration Company) at a 3.02x multiple, the firm aims to shift the balance of power.

We wanted to dig deeper and understand the full story. Here is our conversation with Charles Beigbeder, Founding Partner of Expansion and Audacia.

The feeder – Geodesic

To make this investment sector accessible to all — a first in Europe — Charles launched, through Audacia, a feeder fund named Geodesic. This vehicle allows investors to co-invest alongside the EIF and Bpifrance in advancing Europe’s space sovereignty.

The fund’s distinctiveness lies in its structure: from day one, investors are exposed to Expansion’s existing portfolio, alongside leading French family offices. Moreover, the fund already shows a realized performance of 1.26x, not reflected in the entry price.

In practice, investors support companies such as ReOrbit (smart, reconfigurable satellites), LookUp and Aldoria (space surveillance), HyPrSpace (hybrid propulsion for launchers), and Latitude (micro-launchers).

A way to back a strategic industry, maximize performance, and reinforce Europe’s geostrategic independence.